Will “startups acquiring startups” continue at the same pace?

Selling your startup to another startup has been a viable early-stage exit strategy. Over half of all acquisitions were venture-backed companies buying other venture-backed companies during the halcyon days of 2021, and there are good reasons to do these deals. But is this trend set to continue with a slowdown in later-stage venture capital?

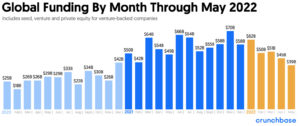

The drop off in VC funding this year has been dramatic, from $62B in January down to $39 million in May. In addition, the impact has been greater for later stage investing, which has fallen by close to 40% compared with equivalent months in 2021. This is consistent with the “trickle down” of the impact of valuations of listed stocks progressively down to Pre-IPO, later-stage and then early-stage investing, as per our article Venture capital and the era of inflation of 13 March.

While organic growth is still important, startups that acquire other startups are well-positioned to achieve their goals faster. In fact, founders who grow their business through acquisition are twice as likely to experience sales growth above their industry average than those who grow organically.

While achieving economies of scale is one of the oldest business models in the books, it acts as a catalyst for startup growth. When a startup acquires another startup, imperative gaps across operations can be filled.

As we all know, locking down top tech talent is one of the biggest challenges for startup founders. Being able to inspire new team members to believe in your startup’s vision and plug in teams who have already been vetted for skills — and know exactly what the startup hustle is all about — is a huge win for companies today.

Two startups can leverage the power of sharing intellectual capital. By coming together to share knowledge, solutions and proof of concepts, there are immeasurable benefits for the operational and financial performance of the company.

To answer the question as to whether the startup acquisition activity will continue, one has to look at the sources funding for these acquisitions – venture capital and venture debt. The drop in the availability of later-stage venture capital will no doubt have an impact.

The case for venture debt funded acquisitions is alluring. It is “virtually” non-dilutive to shareholders, can be used to acquire revenue from the acquisition, which is then leveraged on a multiplier of revenue to increase the valuation for the subsequent funding rounds or an exit. See our article Venture debt could work for you (especially in these times). It will be interesting to see the trend regarding the availability of venture debt.

The “startup acquiring startup” trend is bound to drop off somewhat due to the reduction in particularly later-stage venture capital, but hopefully not to the same extent, as there are still great reasons to acquire startups.