Venture debt could work for you (especially in these times)

Venture debt in its classic form is used by VC-backed startups to leverage their existing VC equity investments, relationships and investability in a variety of situations, including providing extra runway to the technopreneur during a pandemic.

The characteristics of venture debt are driven by its working in combination with venture capital (the size of the venture debt investment in a company can be up to 1/3 or even 1/2 of equity venture capital invested), with less reliance on balance sheet and covenants. Therefore most venture debt providers are happy to support cash flow negative companies; however they look for signs that the company has either a sufficient cash cushion to make debt repayments until it hits profitability (therefore also looking back at recently raised capital) or is in good shape to attract the next round of equity financing.

The main advantage of venture debt is that it is “virtually” non-dilutative. It does not create a valuation event, which is useful in some cases, and certainly simplifies the discussion when valuation is not on the agenda. Venture debt is “signal neutral”, which may be helpful in a situation where there may be a need to prevent a bridge round (a small round of funding to tide a startup over until its next larger round of funding) from existing investors to get the business to the next equity round without showing any alarming signs. Venture debt can also usually be raised in a much shorter time than VC equity.

Some of the situations in which venture debt can be really useful to the technopreneur include:

- Extending the cash runway of your startup to get it to the next “value creation” milestone resulting in a higher valuation at the next equity round.

- If you’re concerned that it might take longer than expected to hit your next milestone and you don’t want to raise equity under unfavourable conditions, venture debt can also be used as an “insurance policy”, allowing you to extend your runway. With the negative effect of Covid-19 looming over the capital markets, this becomes one of the main reasons to consider venture debt.

- Improving the efficiency of an existing round, by raising part of it in debt and reducing dilution for the founders and existing investors.

- Funding an acquisition to accelerate growth.

- Acting as a bridge to profitability.

Venture debt is a fixed term loan (ranging from 12 to 48 months), ranking as senior debt, and with repayments that are highly negotiable from repayment of the loan and capitalised interest at the end of the period, to monthly payments of principal and interest, or anything in-between. There is usually a requirement for collateral, such as a lien on assets, IP or the company itself. But it does not usually have restrictive covenants such as limits on the operations of a company.

Venture debt providers expect returns of 12–25% on their capital but achieve this through a combination of loan interest and capital returns, most often in the form of warrants.

Warrants give venture debt providers an option to subscribe to a predefined amount of a company’s new equity (usually equal to anything between 5-20% of the overall facility) at an exit event — i.e. when the company is sold, merged or listed on an exchange. The price at which options are exercised is agreed at the time of underwriting the facility and is usually linked to the most recent equity round — and if the company grows, venture debt providers partially participate in potential equity upside. However, the dilution from warrants is most often limited to 1-2%.

On occasion, the provider may also seek to obtain some rights to invest in the borrower’s subsequent equity round on the same terms, conditions and pricing offered to its investors in those rounds

Venture debt is provided by some commercial banks with venture lending arms and specialty venture debt funds, with the latter often more flexible on terms. The ideal venture debt investor will have a “light touch” approach to financing. It’s much easier to take money from those who don’t take board seats, take no financial covenants and have very limited governance requirements.

New venture debt business models are emerging. For instance Clearblanc provides venture debt of between £10k to £10 million to ecommerce companies, based on their revenue, where a percentage of their monthly revenue is used to pay back the loan plus a 6-12% fee.

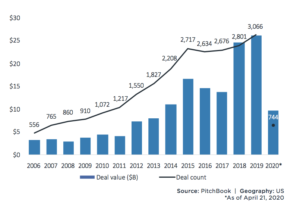

So how widely is venture debt used? Some $25 billion of venture debt was deployed across 3,066 transactions in the US during 2019, accounting for 15% of all venture financing that year. Meanwhile, in Europe, only 5% of all venture financing is in the form of venture debt with the market estimated to be close to $1bn (with Eastern Europe closer to 3%), according to Deloitte.

Venture debt is an actively emerging form of venture funding that is targeted for VC-backed businesses looking for additional funds to fuel growth. Venture debt is also very much relationship driven — since it is a complement to equity capital, it is important that technopreneurs and investors alike are aware of it and build relationships with venture debt providers early on. A smart infusion of debt financing might significantly boost a startup’s growth potential and/or boost the value of the technopreneur’s shareholding.