Fintech M&A 2022 defying gravity

While global M&A and Fintech funding has suffered in 2022, the Fintech sector saw M&A activity rise sharply this year.

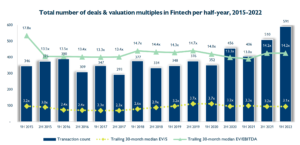

There were 591 Fintech M&A deals recorded in the first half of 2022, representing a 46% increase on 1H2021 numbers, and an even bigger increase of 70% on pre-pandemic (1H2019) figures.*

In contrast, global Fintech funding for the full year 2022 is projected to be 60%, with deal activity to be 73%, compared with 2021, according to CB Insights’ State of Fintech 3Q2022 report.

Also interesting is that Fintech M&A valuations have remained steady: 1H2022 saw the trailing 30-month median revenue multiple reach 3.1x which broadly in line with the levels seen in the past two years. The trailing 30-month median EBITDA multiple came in at 14.2x, firmly within the 13x to 15x range monitored since 2015.*

* Source: Hampleton Partners M&A Market Report 2H2022 Fintech

Until now, macro-economic factors such as inflation, supply chain and geo-political risk have not had a negative effect on Fintech M&A activity. The fundamental drivers of M&A are still in place for the Fintech sector – to acquire new capabilities, enter new markets, expand and to dispose of certain assets to cut costs or sharpen focus.

The majority of acquirers in 2022 have been strategics (69%), although Private Equity (PE) funds, many of whom still have dry powder, account for 31%, which is consistent with the historically narrow range of 30-33% over the last few years.

Only 5% of Fintech M&A transactions announced value above $100 million in 1H2022*, so many of the them are below the radar. Some of the more prominent 1H2022 Fintech M&A deals in the headlines, and as reported by FT Partners, include:

Financial Management Solutions: Anaplan ($10.7Bn PE), Avalara ($8.4Bn PE), ForgeRock ($2.3Bn PE)

Banking & Lending Tech: Black Knight ($15.8Bn Strategic)

Payments: EVO Payments ($4 Bn Strategic) MoneyGram ($1.8Bn PE), Finaro ($575m Strategic)

Wealth & Capital Markets Tech: BetaNXT ($1.1Bn PE)

Crypto & Blockchain: Finfront Holding Company ($1.5Bn Strategic), Bitcoin Depot ($755m Strategic)

InsurTech: BGL ($540m Strategic), Verisk ($515m Strategic)

Healthcare Payments/IT: Signify Health ($8 Bn Strategic), Change Healthcare (claims editing business) ($2.2 Bn PE), Convey Health Solution ($1.1 Bn PE)

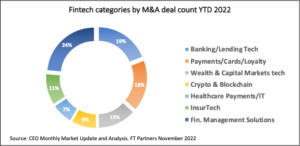

Generally, the categories with the highest number of M&A deals are the most mature i.e. these categories have been attracting funding for longer with more companies having been through progressive funding rounds, namely Financial Management Solutions (24%), Banking/Lending Tech (19%) and Payments/Cards/Loyalty (18%).

Our projection is that Fintech M&A can only increase over the next couple of years, as the reduction in funding means that Fintechs who cannot raise additional funding will be forced to sell to strategic or PE buyers. By the same token, we project that the M&A valuations will decrease slightly, due to the greater availability of Fintech acquisition choices, but with the 30-month median EBITDA multiple probably not dropping much below the 13x EBITDA historical minimum level.