Don’t wait too long to invest in AI

AI investment will set a new record in 2019, but with slowing growth. The sector is starting to mature, and with an ever growing list of AI unicorns, there are great acquisition and IPO opportunities in the sector.

What is AI (Artificial Intelligence) again? Generally we are talking about machine learning, natural language processing and image recognition technologies.

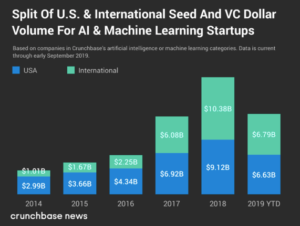

Roughly three-quarters of the way through 2019, it looks like AI funding is on pace to slightly exceed the 2018 total of $19,5, with the big growth between 2016 and 2018.

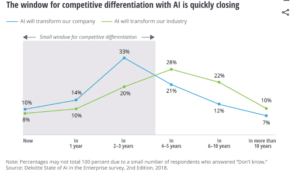

Based on this slowing growth and a Deloitte report that shows that the window for AI competitive differentiation is rapidly closing, we do not expect the current investment levels to continue much beyond the next 3 years or so.

The Deloitte Survey was conducted in 7 key countries (including the US and China) and 1,900 executives from companies that are early adopters in AI.

AI investment can be split into three broad categories:

- hardware infrastructure leveraging demand for new architectures to support AI and machine learning workloads

- tools for developers and data scientists

- applications, running from security to autonomous driving to facial recognition to automating the help desk.

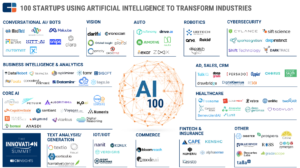

AI investment is spread across industries, but enterprise software, FinTech, robotics, autonomous driving, and biotech boast the largest proportion of well-funded startups.

CVCs (Corporate Venture Capital) accounted for 26% of all AI investment (by value) in 2018 with a total of $5,1 billion in 291 deals, dominated by Baidu (13 investments), Intel Capital (12 investments), SBI Investments (12 investments), GV (11 investments) and M12 (11 investments), according to CB Insights data.

There has been a large shift in the CVC investment geography over the past 5-6 years, with Asian startups accounting for 42% of CVC investment in 2018 versus 4% in 2013. Conversely, CVC investment in US startups went from 94% in 2013 down to 44% in 2018, according to CB Insights data.

We are already on a steady roll of acquisitions. Salesforce’s acquistion of Datorama, a marketing intelligence provider for around $800 million, Blackberry’s acquisition of cybersecurity provider Cylance for $1.4 billion, and S&P’s purchase of analytics provider Kensho for $550 million.

It may be too early to see IPOs given that funding for AI-focused startups really started to ramp up roughly four years ago, however if one looks at the ever-growing list of AI unicorns (listed with the most valuable first), you have got to believe that some of these will IPO in the near future.

Toutiao (Bytedance) (China), SenseTime (China), UiPath (US), Argo AI (US), Face++ (Megvii) (China), Indigo Agriculture (US), Cloudwalk (US), Zoox (US), Horizon, Robotics (US), Automation Anywhere (US) , YITU Technology (China), Uptake (US), BenevolentAI (UK), Avant (US), Cambricon (China), Preferred Networks (Japan), Babylon Health (UK), Afiniti (US), Insidesales.com (US), Graphcore (UK), Pony.ai (US), Darktrace (UK), Dataminr (US), C3 (US), Trax (Singapore), Butterfly Network (US), Infi (Israel), 4Paradigm (China), Outreach (US), TuSimple (US), iCarbonX (China) and OrCam Technologie (Israel).

The AI investment game is already well advanced, with many of the early stage opportunities already snapped up, and with a growing list of later stage companies creating M&A and IPO opportunities. Don’t wait too long to get into the game.

Credit: Crunchbase