Creating personal liquidity by selling shares in your startup

If you have ever tried, as a technopreneur, to sell shares in your startup somewhere in its evolution through to exit, in order to increase personal liquidity, you will know the challenges. However, this is changing with more options emerging, such as marketplaces for the secondary sale of private shares.

This is the first part in a two-part series on secondary sales and private share marketplaces, with the second part digging into the evolution of private share marketplaces and where there are headed.

There could also be other stakeholders interested in the sale of their shares in your startup: A co-founder may have dropped out of the business, employees or ex-employees with vested share options, or early stage seed investors, looking for partial or total liquidity.

Traditionally, a liquidity event such as a capital raise is seen as an opportunity to liquidate shares. This is likely to be more favourably received where the seller is not part of the core team (given that the buyer of secondary shares is also an investor and therefore would like to see the team as committed as possible), and the later the stage of the capital raise.

Series A investors are more likely to want to see the relatively small amounts of money that they shell out being used to grow the business rather than for cash-out, although they may be more amenable to buying the shares of a seed investor than a core team member. The logic changes in later rounds where private equity investors would perhaps like a larger deal size and shareholding (with the investment round already fully subscribed), and when there is an inclination to clean-up the cap-table of multiple tiny shareholders.

Conversely, a new investor may actually use an offer to founders to liquidate some of their shareholding as a differentiator in a competitive situation where the investment is in strong demand. Generally, it is probably fair to say that the likelihood of secondary sales to new investors increases with the competitiveness of the round.

There is also a logic for new investors to purchase some secondaries of key team members to ensure that they are financially stable, perhaps after years of the founders investing their own cash and drawing below-market salaries (but without having founders losing their focus due to the liquidity).

Besides new investors, likely buyers are existing shareholders, who already know and are comfortable with the company, the company itself, private investors (who may also join together to create an SPV), and specialised funds buying secondaries in later stage startups such as Industry Ventures.

The good news is that marketplaces for private shares, are becoming more commonplace as a venue for early stage stakeholders to liquidate shares, particularly in the US, and to a lesser extent, in the UK and Hong Kong.

Forge (founded as Equidate in 2014), and SharesPost (founded in 2009) merged in November 2020 with a combined transaction value of $7.74B, and close to 200 employees across five offices, including New York, San Francisco, and Hong Kong. If you are in the US, you might want to look at EquityZen, MicroVentures and AngelList.

In the UK you could look to AngelList, and crowd-funding sites Seedrs and Crowdcube (separately now that the merger of these two companies is no longer going ahead), all of whom provide a venue for the secondary sale of private shares.

As a seller, one needs to first check the contractual/legal situation relative to the rights of the company, such as:

- Does the company need to first approve the sale of shares? (This has become more common since the Facebook 2011 pre-listing secondary activity debacle where the company lost control of who owned what shares)

- Does the company have a first right of refusal in buying your shares back?

As a buyer of secondaries, one needs to check that:

- The company is prepared to make sufficient information available for you to make a good investment decision. In some cases the company may not be interested in cooperating

- The other shareholders in the company have waived their pre-emptive rights to buy the shares that are on offer, otherwise you may end up putting in a suitable offer, and not getting the transaction done

- Any restrictions and lock-up periods that come with the shares are disclosed

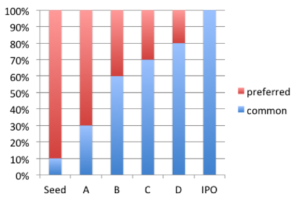

- The other classes of issued shares in the company. Ordinary shares would typically be valued at a discount to preferred shares, taking into account that preferred shares would be paid back their initial investment before the pro-rata liquidation distribution. As a company gets more valuable and closer to an IPO, this discount would reduce, as per the graphic provided by Riz Virk and published on Medium, showing the relative value or ordinary shares (common stock) versus preferred.

Of course a good marketplace can facilitate these disclosures and the provision of suitable information, enabling the technopreneur and other sellers, together with buyers, to more easily navigate this sales process. Beyond that, a good bet would likely still be the sale of your shares to new investors in a later-stage round.