Beware of zombie startup investors in 2025

Technopreneurs should be aware that up to half of the startup funds that existed at the peak of the investment bubble are now zombie investors, unable to make investments in new startups, and are advised to adapt their capital-raising strategies for the changing VC market structure. What is happening in the market, and where is it going?

What exactly is a zombie investor? According to a Pitchbook measure, it is a fund that has not made a new investment in the previous 12 months. This is usually due to running out of dry powder. However, these funds can continue to operate for years as zombies, managing their existing portfolio and collecting management fees.

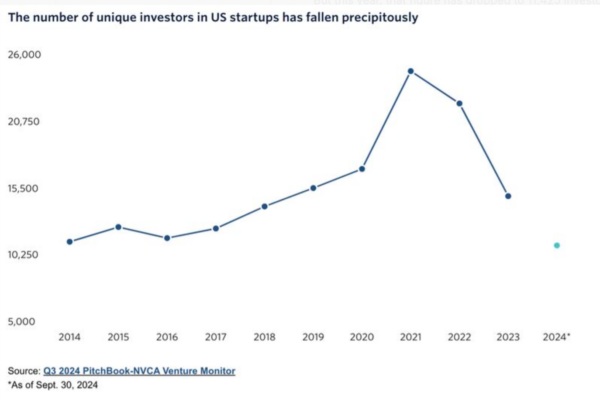

The scale of the decline has been striking, led by the US, where the decline started in 2022, and the extent has been the greatest – down 54% from 25,133 unique investors in 2021 to 11,425 now. This is the lowest number of unique investors in the US in a decade.

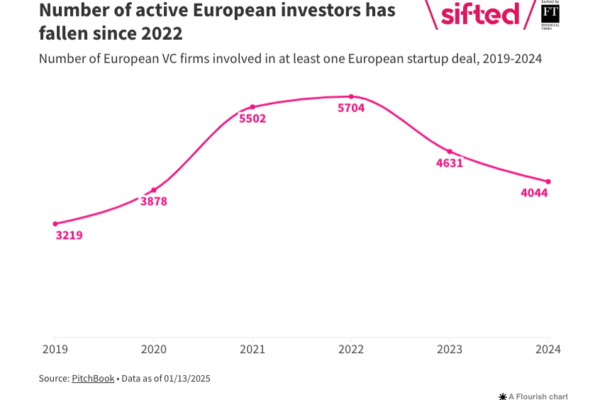

Europe lagged with the decline starting in 2023 and, therefore, not yet to the same extent – down about 30% from a peak of 5,704 in 2022 to 4,044 now. This trend is expected to continue into 2025.

This is a hangover from the heady days when it was much easier for new entrants to raise funds without a track record, combined with the difficulty in achieving exits since then. This has been across the board from seed investors to late-stage investors, with the recent trend of more mature startups eschewing IPOs in favour of private capital. This has made it difficult for many funds to raise further Limited Partner capital.

It seems like the VC market is experiencing a proper shakeup. There’s been a lot of speculation recently about how the VC market will eventually bifurcate into small, specialised firms and big firms with multiple partners and increasingly numerous, large funds.

“I believe you will have institutional investors who look for established brands, track record, a certain amount of safety, and then, on the other hand, solo GPs or small structures that can be more exciting, more volatile, (and provide) more outsized returns, which takes a certain appetite for risk,” according to Jan Miczaika, partner at multi-stage VC HV Capital.

Miczaika thinks it will be the mid-sized firms of between €100-300m that will “have issues”, within the European context. It’s a sentiment echoed by Oliver Holle, CEO and managing partner of early-stage VC Speedinvest in a recent interview with Sifted.

This shakeup will not make it any easier for technopreneurs, who will need to adapt their capital raising strategies with the reduction in the number of mid-sized investors in mind.

Sources:

The number of active VCs in Europe has dropped by 30% in the last two years published by Sifted

PitchBook-NVCA Venture Monitor