The Real-Time Payment Revolution

The world is developing a taste for real-time payments, and there is no going back! Real-time payments are having a disruptive effect on the banking landscape, with very significant benefits to consumers and businesses – reducing transactional risk, improving cash flow and back-office efficiencies, facilitating real-time data analysis and opening the way for new products and user experiences. Ultimately real-time bank payments at the POS have the potential to completely revolutionize the payment landscape.

New entrants with new business models and wallet-based propositions have been the pioneers providing this new taste, in both developed and developing markets, particularly in peer-to-peer (P2P) services. Prominent examples include US-based Venmo, PayPal, China-based WeChat, UK-based TransferWise and Kenya-based M-Pesa (“mobile money” schemes driven by mobile operators in developing markets).

The problem is that we still experience the normal delays in transferring money between our bank accounts and the wallet in question, and we still need our banks for other payment services such as bill payment.

Ideally, we should be able to manage all our payment services from a single transactional account without having to maintain balances in other wallets. For instance, this could be a bank account for a person in a developed market, or a mobile money account for an unbanked person in a developing market. Real-time bank payments have the potential to position the bank account back at the heart of payments for both consumers and businesses.

What are real-time or instant payments?

The Accenture report “Real-time payments for real time banking” lists the following characteristics as common across all real-time payment systems:

- 24×7 availability—consumers should be able to make or receive a payment at any time of day or night, any day of the week.

- Immediacy—the funds being transferred should be available in the recipient’s account in real-time or near real-time.

- Irrevocability—once a payment has been received, it cannot be revoked.

- Certainty—both payer and recipient must be notified in real-time that the payment has been accepted or rejected by the recipient’s bank.

- Richer data standards— most real-time payments schemes across the world standardize data sets to enable greater interoperability, improve payment efficiency and carry richer information with the payment. ISO 20022 is increasingly becoming the standard for financial processing, including for many of the new immediate payment systems.

- Alias/proxy/tokens—In parallel to the demand for immediate payments, there is demand to proliferate ways to connect and transfer funds real-time between parties in the digital economy. This requires the use of addressing databases linking aliases such as mobile phone numbers, email addresses, social media ids, or virtual account numbers to bank account information. Paym in the UK is an example of this.

State of Play

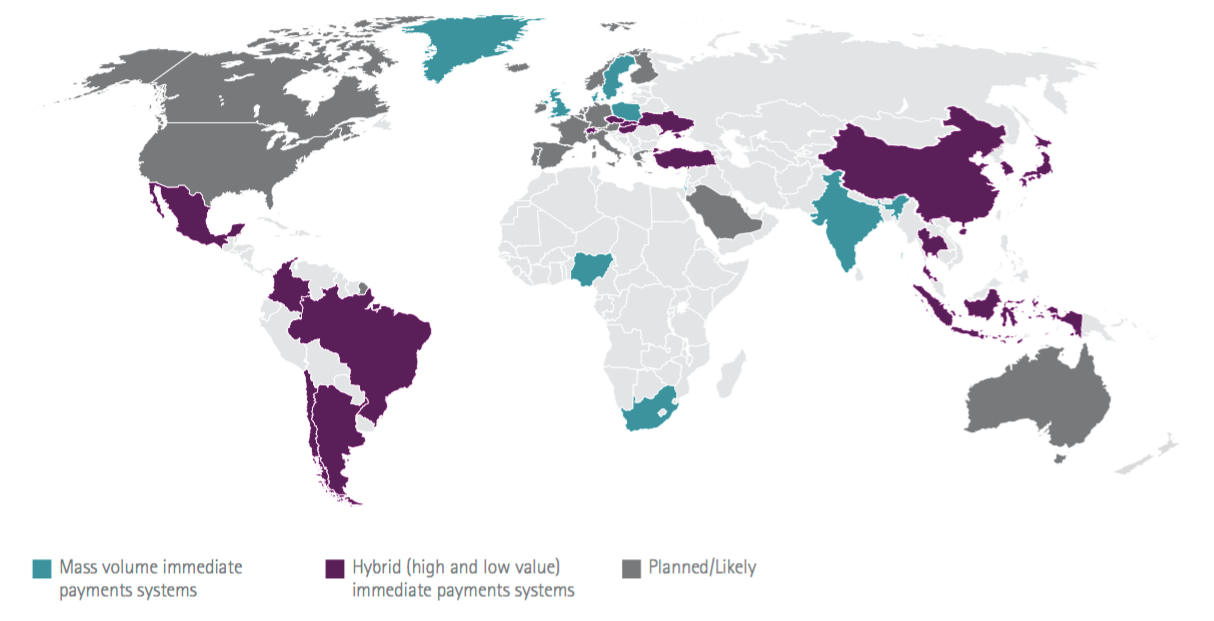

Bank-to-bank real-time payments are not new and have been in use in Japan since 1973, but widespread adoption across several markets is only taking place now. A dozen markets have implemented these since 2001, with the UK, Singapore, South Africa, Mexico and Chile being the more prominent examples based on the widespread use of real-time payments in their respective markets. Today, there are at least 20 additional markets implementing or planning to implement real-time payments.

Together, the US and European Union account for 46% of the global economy. Implementation of cross-border instant payments is being mandated in Europe, with the European Payments Council target for late 2017. The US has not such regulatory push and is therefore expected to take 3-5 years before widespread implementation. In South Africa, the banks came together in 2005 to set their own standards for implementation, in cooperation and with the approval of the Reserve Bank.

The solutions implemented in these two regions will set the standards for future global rollouts. Europe has decided to adopt ISO 20022, and while solutions in the US are still under development, they are likely to adopt the same standard as well.

Interoperability between different payment networks (domestic and cross-border) will grow gradually, driven by competition, converging capabilities and more mature standards. We are likely to see big differences in speed between the different markets driven largely by the local payment cultures.

The Revolution

When real-time payments arrive at the merchant POS, it will provide a credible alternative to existing payment systems, such as the card schemes. If successful, services such as ZAPP in the UK and the NETS EFTPOS service in Singapore that provide payments via bank accounts at the POS will become widespread This is likely to revolutionise the global payment landscape over time.

Sounds amazing..!!!